|

市場調查報告書

商品編碼

1432589

雲端儲存:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Cloud Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

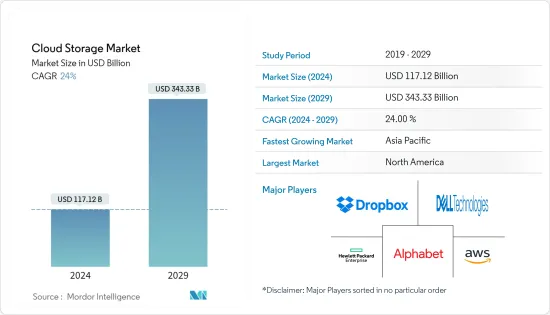

雲端儲存市場規模預計到2024年為1,171.2億美元,預計到2029年將達到3,433.3億美元,在預測期內(2024-2029年)複合年成長率為24%。

所有企業對低成本資料備份、儲存和保護的需求不斷成長,加上處理行動技術使用增加所產生的資料的需求,正在推動雲端儲存的採用率。

主要亮點

- 由於企業資料的增加以及為遠端工作人員提供對資料和文件的無處不在的存取的需要,雲端儲存市場預計將成長。例如,根據 Seagate Technologies Holdings PLC 的數據,從 2020 年到 2022 年,企業資料總量預計將從約 1 Petabyte增加到 2.02 Petabyte。這相當於 42.2% 的兩年複合年成長率。

- 此外,所有企業對低成本資料備份和資料保護的需求不斷成長,以及處理行動技術使用增加所產生的資料的需求不斷增加,催生了雲端儲存。這刺激了雲端儲存的採用。企業經常尋找降低營運成本和提高報酬率的方法,這可以透過外包或僱用第三方供應商的託管雲端服務來實現。

- 透過策略合作、併購和研發,一些市場主要企業已經能夠進一步開發雲端儲存技術。這可能會在預測期內推動雲端儲存需求。

- 在 COVID-19 大流行期間,許多國家出於公共衛生考慮強制要求在家工作,這增加了對遠距工作基礎設施的需求。因此,包括政府機構在內的各級組織都需要滿足對虛擬服務不斷成長的需求以及公民對提供這些服務不斷成長的期望,再形成政府勞動力的長期潛力,使其更具適應性和活力。我們預計廣泛的潛在影響,包括需要提供監管模型。

雲端儲存市場趨勢

BFSI預計將佔較大佔有率

- 為了提高產生收入,銀行可以增加客戶洞察、控制成本、快速且有效率地提供與市場相關的產品,並幫助企業資料資產收益。銀行已開始透過引入線上入口網站來業務數位化,該入口網站允許用戶直接進行業務,而無需銀行工作人員的干涉。結果,資料產生顯著增加,導致這些機構採用雲端儲存。

- 雲端儲存解決方案使銀行能夠同步其企業,打破風險、財務、監管和客戶支援方面的業務和資料孤島,並將大量資料集匯集到一個地方,並與高級分析整合。銀行服務採用該解決方案世界各地的提供者以獲得更好的見解。

- 技術供應商幫助 BFSI 參與者遷移到雲端的措施也推動了該領域的成長。據 Finder 稱,到 2021 年,純專用銀行擁有超過 1,400 萬英國客戶,預計未來幾年將成長 1,000 萬。這表明將需要雲端儲存等解決方案來適應這種成長,從而推動雲端儲存在預測期內的成長。

- 銀行業資料外洩事件的增加正在推動銀行採用雲端儲存。雲端儲存允許資料儲存在由銀行或第三方管理和擁有的空間中,從而為最終用戶提供增強的安全性。因此,雲端儲存的採用預計在預測期內將會增加。例如,根據身分盜竊資源中心的資料,美國金融服務業的資料外洩數量從 2020 年的 138 起增加到 2022 年的 268 起。

預計北美將佔據最大佔有率

- 由於較早採用新技術、對雲端基礎的解決方案的研發投入巨大以及IT基礎設施的加強,預計北美地區將佔據較大佔有率。此外,廉價且安全的儲存選項正在推動產業的快速發展。

- 供應商在北美市場擁有強大的立足點。其中包括 Google LLC、IBM Corporation、Microsoft Corporation、Oracle Corporation、Amazon Web Services Inc. 等。透過研究和開發,該地區的這些主要企業能夠進一步開發其技術。預計這將在預測期內推動雲端儲存的採用並降低雲端儲存成本。

- 根據 Stormforge 2021 年 4 月發布的報告,18% 的北美受訪者表示,他們的組織每月的雲端支出在 10 萬至 25 萬美元之間。此外,44% 的受訪者預計明年雲端支出將增加,另有 32% 的受訪者預計其組織的雲端支出將在明年大幅增加。

- 此外,加拿大政府還採取了「雲端優先」策略,在啟動資訊技術投資、措施、策略和計劃時,將雲端服務確定為主要交付選項並引用。雲端還允許政府利用私人提供者的創新,並使資訊技術更加敏捷。此類措施預計將為混合雲市場提供許多機會,因為這種模型可以實現私有雲端的安全性和公有雲的彈性。

雲端儲存產業概況

雲端儲存市場集中度適中,微軟、IBM、 Oracle等大公司佔有較大佔有率。每家公司的持續創新能力使他們比其他公司具有競爭優勢。透過策略夥伴關係、研發和併購,這些參與者正在市場上留下更大的足跡。

- 2022 年 11 月:作為 Dell APEX 產品組合持續發展勢頭的一部分,Dell Technologies Inc. 宣布 Dell PowerFlex 現已在 AWS Marketplace 上提供。該產品允許客戶在使用現有雲端積分的同時,利用 PowerFlex 的關鍵任務效能、彈性、擴充性和管理。 Dell PowerFlex 是戴爾主要儲存軟體產品中第一個透過 Project Alpine 在公有雲中提供的產品,是 AWS 廣泛的資料保護產品組合的補充。

- 2022 年 5 月:紅帽公司和Accenture擴大其近 12 年的策略合作夥伴關係,為全球企業推動開放混合雲端創新。兩家公司將投資共同開發新解決方案,幫助無縫駕馭多重雲端和混合雲端世界,並將合作制定策略並加快創新步伐,以更快地實現價值。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- COVID-19 市場影響評估

- 過去幾年的成本/價格趨勢分析

第5章市場動態

- 市場促進因素

- 提高整個組織的雲端採用率

- 對更低成本儲存和更快資料存取的需求不斷成長

- 市場挑戰

- 隱私和安全問題

- 技術簡介

- 雲端儲存閘道器

- 主儲存

- 備份存儲

- 資料存檔

第6章市場區隔

- 按模式

- 私有雲端

- 公共雲端

- 混合雲端

- 按行業分類

- BFSI

- 零售/消費品

- 衛生保健

- 媒體娛樂

- 資訊科技/通訊

- 製造業

- 政府機關

- 其他最終用戶產業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章 競爭形勢

- 公司簡介

- Google LLC(Alphabet Inc.)

- Amazon Web Services Inc.

- Dropbox Inc

- Dell EMC(Dell Technologies Inc.)

- Hewlett Packard Enterprise Company

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Rackspace Inc.

- NetApp Inc.

- Alibaba Cloud(Alibaba Group)

第8章投資分析

第9章 市場未來展望

The Cloud Storage Market size is estimated at USD 117.12 billion in 2024, and is expected to reach USD 343.33 billion by 2029, growing at a CAGR of 24% during the forecast period (2024-2029).

The increasing demand for low-cost data backup, storage, and protection across all enterprises, coupled with the need to handle data generated by augmented usage of mobile technologies, favors the adoption rate of cloud storage.

Key Highlights

- The cloud storage market is expected to grow due to rising data volumes across enterprises and the growing need to provide remote workers with ubiquitous access to data and files. For instance, according to Seagate Technologies Holdings PLC, from 2020 to 2022, total enterprise data volume is expected to go from approximately one petabyte (PB) to 2.02 petabytes. This is a 42.2% average annual growth over two years.

- Further, the total volume of data/information created, captured, copied, and consumed worldwide is expected to reach 181 zettabytes in 2025 from 79 zettabytes in 2021. Further, the World Economic Forum estimates that, by 2025, 463 exabytes of data will be created globally, equivalent to 212,765 thousand DVDs per day.

- Moreover, the increasing demand for low-cost data backup and protection across all enterprises, coupled with the necessity of handling the data generated by augmented usage of mobile technologies, favors cloud storage adoption. Companies regularly find ways to mitigate their operating costs and increase profit margins, which can be done by outsourcing or adopting managed cloud services from third-party vendors.

- Through strategic partnerships, mergers and acquisitions, and R&D, some of the prominent players in the market have been able to further develop the cloud storage technology. This may fuel the demand for cloud storage over the forecast period.

- Amid the COVID-19 pandemic, many countries mandated work from home due to public health safety concerns that drove the need for remote working infrastructure. Thus, organizations at all levels, including government bodies, expected a wide range of potential impacts, such as increased demand for virtual services, coupled with rising citizen expectations around the delivery of these services, the long-term potential for reshaping the government workforce, and the need to provide adaptive and dynamic regulatory models.

Cloud Storage Market Trends

BFSI Expected to Hold a Significant Share

- To improve revenue generation, banks increase customer insights, contain costs, deliver market-relevant products quickly and efficiently, and help monetize enterprise data assets; they have started digitizing their work by introducing online portals through which a user can directly meet his work without any requirement for a bank official's intervention. This further results in a substantial increase in data generation, propelling such institutions to adopt cloud storage.

- Banking service providers worldwide are adopting cloud storage solutions as it enables banks to synchronize the enterprise, break down operational and data silos across risk, finance, regulatory, and customer support, and allow institutions to combine massive data sets in one place for advanced analytics and integrated insights.

- Increasing initiatives from technology vendors to help the BFSI players transition into the cloud also fuel this segment's growth. According to Finder, in 2021, digital-only banks had more than 14 million customers from Britain, which is expected to grow by 10 million in the next few years. This indicates that such an increase would require solutions like cloud storage to handle the surge, thereby boosting the growth of cloud storage over the forecast period.

- The rising data breaches in the banking sector are driving the banks to adopt cloud storage that enables them to store data in a space managed and owned by the bank or a third party, providing enhanced security to the end-user. This is expected to increase cloud storage adoption over the forecast period. For instance, according to the data from the Identity Theft Resource Center, the number of data compromises in the financial services sector in the United States reached 268 in 2022, up from 138 such incidents in 2020.

North America Expected to Hold the Largest Share

- North America is predicted to hold a major share owing to the early adoption of new technologies, huge investments in R&D for cloud-based solutions, and enhanced IT infrastructure. Moreover, cheap and secure storage options result in rapid industrial development.

- The North American region has a strong foothold of vendors in the market. Some of them include Google LLC, IBM Corporation, Microsoft Corporation, Oracle Corporation, and Amazon Web Services Inc. Through research and development, these prominent players in the region have been able to develop the technology further. This is expected to boost the adoption of cloud storage and reduce the cost of cloud storage throughout the forecast period.

- According to a report published by Stormforge in April 2021, 18% of respondents from North America stated that their organization has a monthly cloud spend that ranges between USD 100,000 and USD 250,000. Further, 44% expect cloud spending to increase over the next 12 months, while another 32% indicate that they expect their organization's cloud spending to increase significantly over the next 12 months.

- Moreover, the government of Canada has adopted a "cloud-first" strategy, whereby cloud services are identified and estimated as the principal delivery option when initiating information technology investments, initiatives, strategies, and projects. The cloud will also let the government harness the innovation of private-sector providers and thus make its information technology more agile. Such initiatives are expected to offer plenty of opportunities to the hybrid cloud market, as this model enables private cloud security and public cloud flexibility.

Cloud Storage Industry Overview

The cloud storage market is moderately concentrated owing to some major players, such as Microsoft, IBM, and Oracle, holding significant market share. Their ability to continually innovate their offerings has allowed them to gain a competitive advantage over others. Through strategic partnerships, research and developments, and mergers & acquisitions, these players have gained a more significant footprint in the market.

- November 2022: As part of continuing Dell APEX portfolio momentum, Dell Technologies Inc. announced that Dell PowerFlex is available in the AWS Marketplace. This offer provides customers with the mission-critical performance, resilience, scale, and management of PowerFlex with the ability to use existing cloud credits. Dell PowerFlex is the first of Dell's leading storage software offerings to be available in the public cloud via Project Alpine and compliments its broad AWS data protection portfolio.

- May 2022: Red Hat and Accenture expanded their nearly 12-year strategic partnership to advance power-open hybrid cloud innovation for enterprises worldwide. The companies are partnering to invest in the co-development of new solutions to help in the seamless navigation of a multi- and hybrid cloud world, define their strategy, and accelerate their pace of innovation to get to value faster.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Cost/Price Trend Analysis for the Past Few Years

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increase in Cloud Adoption Across Organizations

- 5.1.2 Growing Demand for Low-cost Storage and .Faster Data Accessibility

- 5.2 Market Challenges

- 5.2.1 Privacy and Security Concerns

- 5.3 TECHNOLOGY SNAPSHOT

- 5.3.1 Cloud Storage Gateway

- 5.3.2 Primary Storage

- 5.3.3 Backup Storage

- 5.3.4 Data Archiving

6 MARKET SEGMENTATION

- 6.1 By Mode

- 6.1.1 Private Cloud

- 6.1.2 Public Cloud

- 6.1.3 Hybrid Cloud

- 6.2 By End-user Vertical

- 6.2.1 BFSI

- 6.2.2 Retail and Consumer Goods

- 6.2.3 Healthcare

- 6.2.4 Media and Entertainment

- 6.2.5 IT and Telecom

- 6.2.6 Manufacturing

- 6.2.7 Government

- 6.2.8 Other End-user Verticals

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Google LLC (Alphabet Inc.)

- 7.1.2 Amazon Web Services Inc.

- 7.1.3 Dropbox Inc

- 7.1.4 Dell EMC (Dell Technologies Inc.

- 7.1.5 Hewlett Packard Enterprise Company

- 7.1.6 IBM Corporation

- 7.1.7 Microsoft Corporation

- 7.1.8 Oracle Corporation

- 7.1.9 Rackspace Inc.

- 7.1.10 NetApp Inc.

- 7.1.11 Alibaba Cloud (Alibaba Group)

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

2024-2032 年按元件、部署類型、使用者類型、垂直產業和地區分類的雲端儲存市場報告

2024-2032 年按元件、部署類型、使用者類型、垂直產業和地區分類的雲端儲存市場報告 2024 年雲端儲存世界市場報告

2024 年雲端儲存世界市場報告 全球雲端儲存市場:按產品、用例、部署模型、組織規模、產業、地區 - 預測(~2028 年)

全球雲端儲存市場:按產品、用例、部署模型、組織規模、產業、地區 - 預測(~2028 年) 雲端原生儲存市場規模 -按應用(備份和復原、內容交付、巨量資料和分析、資料歸檔、資料庫儲存管理)、元件、最終用戶產業、企業規模、部署模型和全球預測,2023-2032 年

雲端原生儲存市場規模 -按應用(備份和復原、內容交付、巨量資料和分析、資料歸檔、資料庫儲存管理)、元件、最終用戶產業、企業規模、部署模型和全球預測,2023-2032 年 全球儲存即服務市場規模研究與預測,依服務類型依企業規模依產業垂直與區域分析,2023-2030 年

全球儲存即服務市場規模研究與預測,依服務類型依企業規模依產業垂直與區域分析,2023-2030 年 雲端儲存市場報告:2030 年趨勢、預測與競爭分析

雲端儲存市場報告:2030 年趨勢、預測與競爭分析 2024-2028年全球雲端儲存服務市場

2024-2028年全球雲端儲存服務市場 全球雲端原生儲存市場:按產品、按用途、按行業、按地區 - 預測到 2028 年

全球雲端原生儲存市場:按產品、按用途、按行業、按地區 - 預測到 2028 年 全球存儲即服務市場

全球存儲即服務市場 到2030年的雲端原生存儲市場預測:按組件、組織規模、部署類型、最終用戶和區域進行的全球分析

到2030年的雲端原生存儲市場預測:按組件、組織規模、部署類型、最終用戶和區域進行的全球分析